Mrs. Cardholder

Obtaining citizenship for women in the great state of credit

Happy Wednesday!

In honor of women’s history month, which is every month in my household (just ask the cats), I’ve got a series of three posts about women and property. Today, we kick things off with some legal history about credit rights, gender equality, and the financial services industry.

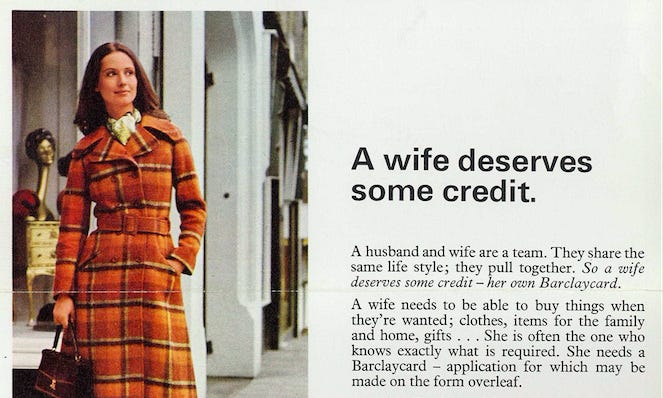

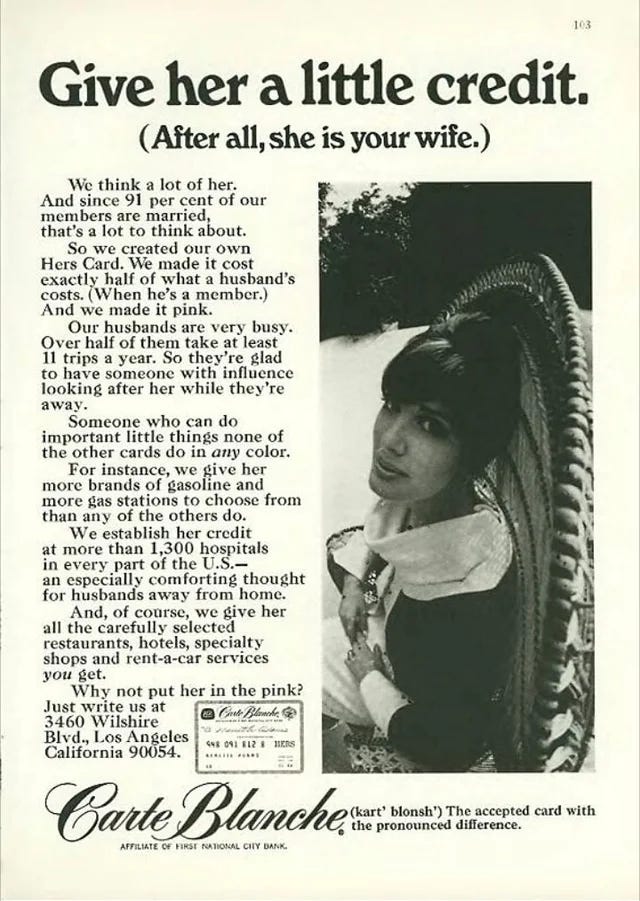

Imagine this scenario: it’s 1970 and Eliza, a woman with a job and her own paycheck, applies for a store credit card to buy a new coffee table. Gold and glass are all the rage. The manager agrees that Eliza is financially qualified based on her salary, but refuses to issue the card in her name because she’s married. Eliza is told that her husband should be the one to apply or that she should apply under his name, as “Mrs. Cardholder.” (It’s 1970, marriage is decidedly heteronormative.)

Eliza’s situation is typical of how married women were treated with respect to credit prior to 1974 and the passage of the Equal Credit Opportunity Act. This legislation prohibited lenders from discriminating against credit applicants on the basis of protected categories, including sex and marital status. The Act was a victory for women and a step forward on the path to gender equality.

But there’s a more complicated relationship between women, equal rights, and credit. One that reveals how deeply profitable the expansion of credit was for the financial services industry, and how discrimination has persisted, even after the Act’s passage.

A brief history of credit discrimination and expansion

Before 1974, women were not legally barred from accessing formal credit, but it was difficult to obtain in practice. Eliza’s situation demonstrates how “creditors routinely cancelled credit cards that women had carried before marriage in their own names and required women to reapply for credit under the husband’s name—with his permission and signature.”1 This reissuing stripped a married woman of her individual financial identity when it came to credit applications and all consumer activity for the household became subsumed into the credit history of the husband.

Married women who were working paid jobs faced discrimination because lenders were afraid they would get pregnant and quit, and lenders routinely asked working women for “pill letters,” swearing that they were using birth control. Single women were also treated with suspicion, since the assumption was that they were surely on the verge of marriage. Divorced women were in possibly the worst situation, with no credit history or steady income to help them obtain credit. All women were living outside of the credit universe, unable to self-actualize in the most socially conventional way, as economic citizens and consumers.

Because of these kinds of discrimination, both the Civil Rights and Feminist movements coalesced around the rallying cry of democratized credit. For civil rights leaders, access to credit was an important issue in terms of both racial and economic justice. For feminists, the matter was equally one of equality and opportunity. Consequently, the passing of the Equal Credit Opportunity Act of 1974 was a watershed moment.

How the financial services industry benefitted

Credit was, in this story, tied to rights, equality, and the dream of a middle-class lifestyle as defined by material comfort. Credit’s downside, debt, was not mentioned in this “good news” message. Also absent from the conversation was the enormous boon that the expansion of credit would bring to the financial services industry: lenders, credit ratings agencies, and debt collectors alike.

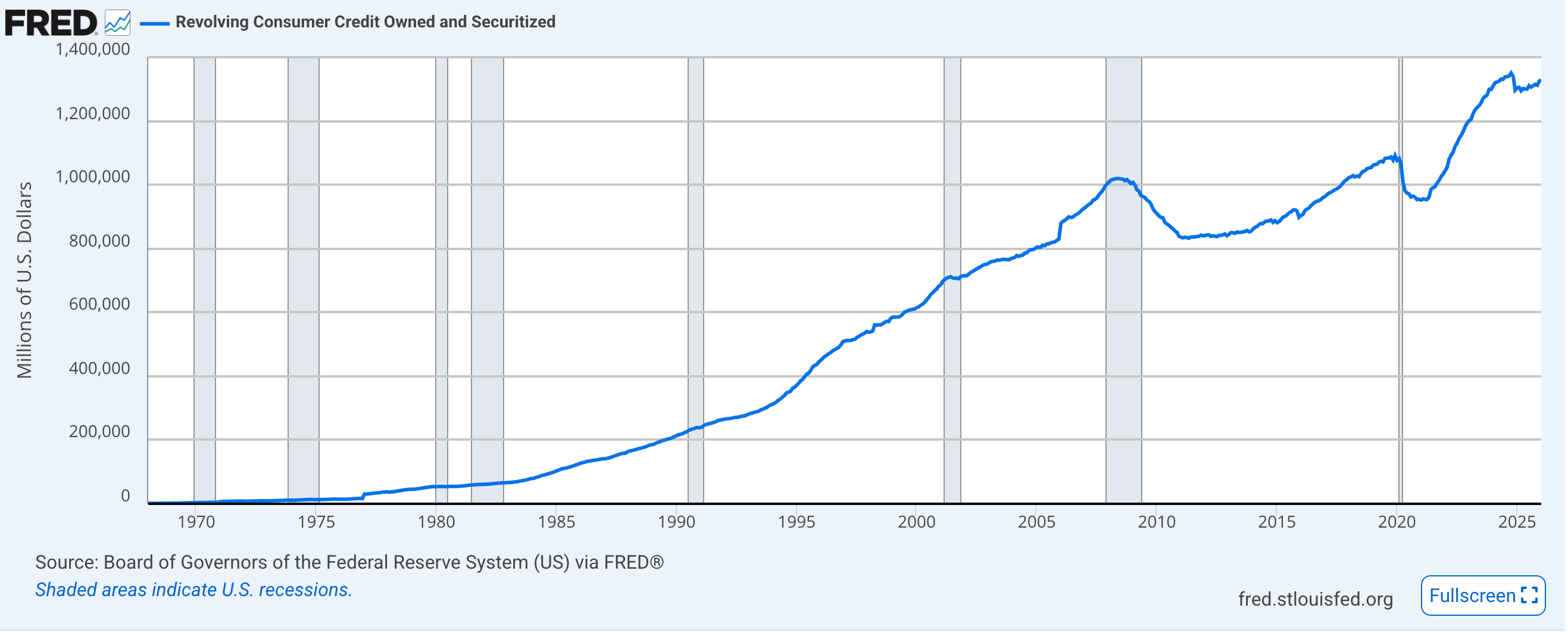

In particular, revolving credit accounts were just starting to take off as equal credit was being discussed by politicians and activist. An expanded consumer base was just what the industry needed to help fully launch their new products. And this is exactly what the provision of new credit rights did. In 1974, the year of the Act’s passage, revolving credit represented about $13.5 billion (about 7% of total consumer credit). By 1980, that number had risen to about $55 billion; by 1990 it was at around $239 billion. (As of January 2026, revolving consumer credit is roughly $1.329 trillion, 27% of all consumer credit.) Credit inclusion was big business.

Why discrimination persisted

Another unintended outcome of the Act was a shift in the workings of discrimination. Barred from looking at gender (or race), credit bureaus took refuge in scoring systems that tracked purportedly objective variables. Discrimination could occur as long as it was based on “non-protected” categories and characteristics. One banking magazine told its readers: “Credit judgments, by their very nature, are discriminatory. You must be ready to prove they are not unfairly discriminatory.”

The problem was that lenders and raters used proxy variables indexed to prohibited categories. Lenders no longer rejected women strictly because of their gender or marital status. They rejected women based on criteria such as gaps in employment, length of employment, and lower incomes as well as lower levels of wealth. Credit decisions were no longer a reflection of obvious discrimination. Instead, credit decisions became “a reflection of real structural inequalities in American society” and bias was almost inescapable since “gender and racial inequities were woven directly into the fabric of American society.”2

The story for women was that credit was a social good to be desired, part of economic citizenship. Equal credit was an unqualified gain. The story of race and credit was the same. In pursuing credit expansion, however, equality advocates turned away from the option to pursue equality through other pathways. Pathways that did not create debt and dependency and that gave women actual resources other than just the ability to obtain revolving credit.

Question: Have you experienced credit discrimination because time off for caretaking, no credit history after a divorce, or other problems that arise out of marriage? Have you heard stories from your mother, grandmother, or other female relatives about credit discrimination? 💸💸💸💰💰💰

If you enjoyed this post, you may be interested in learning more about my forthcoming book, The House that Family Money Built, which discusses geographic concentrations of both wealth and poverty. These posts 👇🏻 are a good place to start.

Greta R. Krippner, Democracy of Credit: Ownership and the Politics of Credit Access in Late Twentieth-Century America, 123 Am. J. Socio. 1, 15 (2017).

Josh Lauer, Creditworthy: A History of Consumer Surveillance and Financial Identity in America 248 (2017).

I remember learning about the 1970 credit act last year, and feeling shocked that so many developments for a woman's independence came so very recently. Reading this line was alarming: "Credit decisions became 'a reflection of real structural inequalities in American society' and bias was almost inescapable since 'gender and racial inequities were woven directly into the fabric of American society.'"

Reminds me of people I know who have had to be very careful with their "identity" in the workplace because it could get you fired under the terms of underperformance.

I was discriminated against applying for my first job after marriage in that employers demanded to know whether I was pregnant and/or if I was soon to be pregnant. As to credit, in a small town, the owner of the department store would simply send the bill to the husband, or he (always he) would call the husband and get his approval to issue a card in the husband's name that the wife could use.

Speaking of small towns, I guess this is sort of related. My husband was appalled when I bounced a check right after we married. I literally had no idea that I was supposed to check the balance before writing a check. In our small town, when I was in college, I would write checks for what I wanted. If there wasn't enough in my account, the banker (a friend) would call Daddy and he would put more money in my account. I thought if I still had checks I had money. As a kid, we would "buy" things as the grocery store and they would send the bill to Daddy.

So, I guess the flip side of the credit story is women were deliberately kept ignorant of credit and money in general. Note how this ignorance reinforced certain stereotypes about women. Funny how that works.